With the S&P 500 up over 140% in the past five years, it’s getting harder and harder to find stocks worth buying and holding for the long-term at current prices. The value investor in me loves to find great companies trading at a low P/E ratio, but those companies are few and far between as of late. But sometimes uncovering good companies requires a little bit of digging.

I love investing in banks because the business model of a bank is (at least it should be) very simple, and the services that banks offer will always be in demand. As I mentioned in my last post, I have seen unbelievable returns from my investments in Bank of America, Citigroup, Bank of Ireland, Morgan Stanley, Fifth Third Bancorp, and Southwest Bancorp over the past five years. But, with all successful trades, there comes a price at which it is time to ring the register and sell, and, aside from the extremely reduced position I am still holding in IRE, I sold my shares and cashed in on all of these banks long ago.

But I am still holding a large position in one bank- the bank that I believe to be “best in breed” of all the U.S. megabanks and the one I believe is the safest long-term investment. On the surface, Wells Fargo may not seem like the best bet of the big banks from a value perspective. With a P/E ratio of about 13 and a P/B ratio of about 1.7, WFC is far from exciting. However, Patrick Morris at The Motley Fool does an excellent job of pointing out how great Wells Fargo is compared to its peers.

Morris highlights several important valuation metrics for banks. In the article, he looks at WFC’s return on average assets (the profitability of a company’s assets), return on equity (how much profit a company generates with its shareholders money), and net interest margin (how well a company’s investments perform when compared to its debts). When compared to its peers, WFC is performing at a much higher level. But if you are looking for more convincing than Mr. Morris provided, let me take a crack at it.

I recently posted about the fact that the financial crisis that occurred in 2008 hit the banking sector hardest of all, with several large banks failing and other large banks barely surviving with the help of government bailouts. This crisis, by the way, occurred because of the reckless behavior of many of these banks to begin with. But not all of the banks were behaving badly. And a very simple way to see which banks were behaving the worst is to look at the market capitalizations of the banks before the crisis and compare them to current market caps. The “bad banks” responsible for the crisis had to pull out all the stops to avoid bankruptcy, which often included selling assets. The “good banks” were able to take advantage of the opportunity to actually expand and grow their businesses, much like traders such as myself were able to take advantage of the crisis to achieve incredible gains.

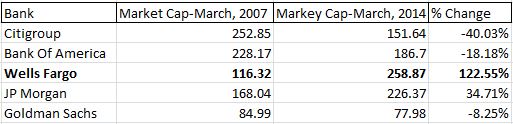

Take a look at this table of the market caps (in $billions) of these five banking sector giants compared to what they were seven years ago:

To me, the change in market cap is the single most telling metric when looking at the performance of each of these banks over the last seven years. Citigroup, Bank of America, and Goldman Sachs are all smaller than they were in 2007. JP Morgan is larger by about a third. Wells Fargo has more than doubled in size during the most severe financial crisis since the Great Depression. Game, set, and match.

Finally, as a true value investor at heart, the cherry on top of my WFC position is that the most famous value investor of all time, Mr. Warren Buffett, currently holds WFC as his largest position, and, as Patrick Morris pointed out, Buffet is still adding to his WFC position. I bought WFC just about a year ago at $37.75, and so far I am up about 33% on my investment. WFC has grown to be my third largest holding, and I have no plans on selling any time soon!

If your eyes glazed over when I mentioned “net interest margin,” fear not! My book, Beating Wall Street with Common Sense: How I Achieved a 400% Return from my Dorm Room, contains an entire chapter devoted to explaining the mysteries of value investing!