This week, the S&P 500 cut through the 1900 level like a hot knife through butter. As each new numerical milestone falls, investors are left wondering whether this bull market is reaching its pinnacle. Unfortunately, there’s no certain way to know when a market is reaching a top or bottom. However, one person that has a stellar track record of predicting market tops is Yale economist and Nobel laureate Robert Shiller. In this article, I am going to use Shiller’s CAPE metric to take a look at the current bull market and three of the largest megacap stocks, ExxonMobile Corporation (NYSE: XOM), Johnson & Johnson (NYSE: JNJ), and General Electric Company(NYSE: GE).

The CAPE crusader

In March 2000, Robert Shiller released his book Irrational Exuberance at the very height of the dot-com bubble. On several occasions between 2003 and 2007, Shiller published papers and made public predictions of the collapse of the housing market. [ ] In Irrational Exuberance , Shiller often references CAPE, which is an acronym for “cyclically adjusted price-earnings.” That may sound impressive, but all Shiller has done with this metric is tweak the denominator in the familiar price-to-earnings (P/E) ratio. Instead of using the previous four quarters of earnings, Shiller uses an average of the previous 10 years of earnings. This simple modification smooths out the earnings number and eliminates the influence of short-term earnings fluctuations.

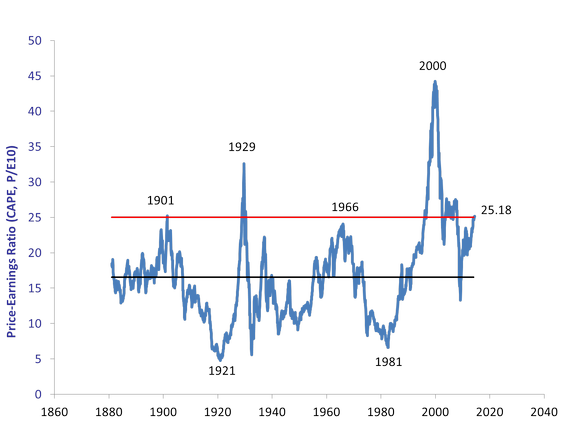

So when you take the CAPE for the S&P 500 throughout history and adjust for inflation, you get this graph:

[ ] The blue line shows how CAPE for the S&P 500 has fluctuated over time. The black horizontal line I added represents a CAPE of 16.5, which is the mean historical CAPE. The red line represents a CAPE of 25 and is included because the CAPE recently crossed above 25 for the first time since early 2008.

A history lesson

It’s clear that the current CAPE is well above its historical mean of 16.5. But since 1881, the S&P’s CAPE has been above 25 (the red line) only 8.9% of the time .

In fact, the CAPE has only crossed above the 25 level four other times in history. The first time was in June 1901. From June 1901 to November 1903, the Dow Jones dropped more than 46%. [ ] The next time the CAPE crossed above 25 was November 1928. Of course, “Black Tuesday” occurred about one year later, and from mid-1929 to mid-1932 the Dow dropped 96% as the Great Depression set in.

After the Great Depression, the CAPE remained below 25 for decades until December 1995. At the height of the dot-com bubble, the CAPE peaked at over 44 in December 1999. When the bubble burst a month later, the Dow dropped about 20% from January 2000 to March 2001. The most recent time the CAPE pierced the 25 level was in the end of 2003 during the housing bubble. We all remember the financial crisis that resulted, and the subsequent 50% drop in the Dow from 2007 to 2009.

What can CAPE tell us about three megacaps?

Since a graph of CAPE requires 10 years of earnings to get a single data point, only certain companies can be analyzed using the metric. Any relatively new company that is experiencing rapid earnings growth will have its CAPE inflated from its past earnings, and the number might not accurately reflect the modern company. For example, Apple’s current CAPE of 39.5 seems extremely high. However, 10 years of Apple earnings stretches back to 2004, a time at which the iPhone and iPad were nothing more than twinkles in Steve Job’s eye.

But CAPE can tell us a bit about blue chip companies like GE, Exxon, and J&J:

Since these three giants are from different industries, it’s hard to compare apples to oranges. However, CAPE can give some perspective on how expensive these stocks have been over the past 10 years. For example, all three companies’ current CAPEs are lower than their respective mean 10-year CAPEs. However, despite the major bull market of the past few years, Exxon’s current CAPE of 15.1 remains near a 10-year low and is below Shiller’s historical mean CAPE of 16.5 for the overall market. While none of these companies seem to be exhibiting bubble-like spikes in CAPE, Exxon’s low CAPE coupled with a return on equity (ROE) of 24.3% and a tiny 0.12 debt-to-equity ratio [ ] makes the company look like the safest bet of the three at these levels.

CAPE’s limitations

While CAPE is certainly a helpful way to keep tabs on how expensive stocks are, it has its limitations. For example, CAPE gives no indication of exactly when a peak will occur. If you had sold all your stocks when the CAPE reached 25 in 2003, you would have sold when the S&P 500 was at 1000. You certainly would have avoided the market crash in 2008/2009, but you would have been waiting for it to happen for about four years, and you would have missed the more than 50% rise in the S&P to its peak of over 1500 in October 2007!

So with a current CAPE of 25, are stocks expensive? Yes. Is a market correction coming at some point ? Almost certainly. Does the current CAPE above 25 means we the end of the bull market is imminent like it did in 1928, or will we see another 50% rise in the market like we did from 2003 to 2007? Only time will tell.

Want to learn more about how to analyze stocks? Or maybe you just want to be able to look sophisticated in front of your coworkers when they ask you what you are reading on your Kindle, and you’d prefer to tell them “Oh, I’m just reading a book about stock market analysis,” rather than the usual “Oh, I’m just looking at pics of my ex-girlfriend on Facebook.” For these reasons and more, check out my book, Beating Wall Street with Common Sense. I don’t have a degree in finance; I have a degree in neuroscience. You don’t have to predict what stocks will do if you can predict what traders will do and be one step ahead of them. I made a 400% return in the stock market over five years using only basic principles of psychology and common sense. Beating Wall Street with Common Sense is now available on Amazon, and tradingcommonsense.com is always available on your local internet!

[ ]