Yesterday I wrote about beta and discussed how it is calculated and what it means. But unless you know how to use beta to your advantage, it’s no more than a fun fact.

Risk management is one of the major themes of my book. I specifically address age as one important factor in determining the appropriate risk level for each person’s portfolio:

I was 24 years old when I bought my fist shares of stock with my laptop in my dorm room. In 2008, I invested a large portion of my life savings in the stock market. While I felt that I had a very good chance to make excellent returns in a relatively short period, I had two major advantages working for me. The first advantage is that my 24-year-old-college-student life savings were not very large. I didn’t have too much to lose, even if I had lost it all. The other advantage is time. If I needed to, I could have waited 30 years (God willing) to sell my stocks. Even if the United States had gone into a decade-long depression, as long as it made it through in the long run I would have come out of it none the worse for wear. If you happen to be young like me, take advantage of time being on your side. You can afford to be more aggressive with your strategies. Certainly don’t be reckless, and do not borrow money to invest, but if you trade away your life savings, so what? Young people can afford to start over. If you blow your retirement money in the market when you are 58 years old, you do not have time to recover. Whatever your age, weigh your risk according to how much money you can afford to lose. If you can handle the worst-case scenario, you can certainly handle all the other ones.

But age is certainly not the only factor that goes into determining how much risk is appropriate for you. Do you have a family? Kids? Do you have an appropriate level of financial security? Do you have trouble sleeping at night because you are worried about the stock market? Everybody is different, and one of the best things about managing your own money is that you have total control and can completely tailor you investment strategy to suit your situation.

Back in 2008, I was chomping at the bit to buy stocks, and yet lately I have been much less enthusiastic. So have I just gotten more risk-averse at the ripe old age of 30? Those that know me best emphatically know that’s not the case. But the stock market environment has totally changed in the last six years, and the exact point in the market cycle is another extremely important factor for determining an appropriate risk level.

So for me personally, I have been concentrating lately on balancing these two opposing forces: I’m young and willing to be aggressive with my investments, but the market environment does not seem particularly appealing at the moment.

Paul La Monica suggests that now is the time to invest in “safe” stocks. But that’s not what I’m doing.

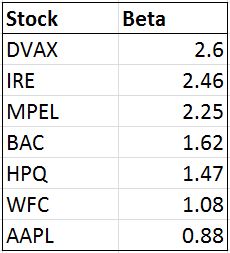

Here’s a list of all the stocks I’m currently holding long along with their current betas.

As I explained yesterday, a beta of less than 1 means that the stock is less volatile than the overall market, and a beta of greater than 1 means a stock is more volatile than the overall market. Sooooo six out of my seven stocks are more volatile than the overall market? It doesn’t sound like the best approach to a “scary” stock market.

But there’s more to risk management than owning nothing but low-beta stocks at all times. For example, Apple, my lowest-beta stock, is also my largest holding. It contrast, Dynavax and Bank of Ireland, my two highest-beta stocks, are my two smallest holdings. In fact, my combined stakes in Dynavax and Bank of Ireland are still less than half the size of my position in Apple. So balancing beta is one important aspect of risk management.

But since I do have such a long-term investment horizon, rather than managing risk by moving my cash into low-risk stocks, I’ve simply moved my cash into… cash.

I know no matter what happens in the market, my cash is safe. Sure, I could be selling all my high-beta stocks and buying low-beta stocks. But I’d rather maintain my positions in the high-beta stocks and simply reduce the size of the positions, which is what I have done with many of my positions over the past year or so. I know that eventually the market will provide another opportunity to buy some high-beta stocks for cheap (it always does…), and I’ll be there waiting with my finger on the trigger.

Want to learn the other factors you need to consider when determining the appropriate risk level for you? Or maybe you just want to be able to look sophisticated in front of your coworkers when they ask you what you are reading on your Kindle, and you’d prefer to tell them “Oh, I’m just reading a book about stock market analysis,” rather than the usual “Oh, I’m just looking at pics of my ex-girlfriend on Facebook.” For these reasons and more, check out my book, Beating Wall Street with Common Sense. I don’t have a degree in finance; I have a degree in neuroscience. You don’t have to predict what stocks will do if you can predict what traders will do and be one step ahead of them. I made a 400% return in the stock market over five years using only basic principles of psychology and common sense. Beating Wall Street with Common Sense is now available on Amazon, and tradingcommonsense.com is always available on your local internet!