Hewlett-Packard released their quarterly earnings last week, and the market’s reaction to the news has been awesome so far for shareholders like me. The company produced earnings that were in line with expectations and issued forward guidance that was at the high end of the expected range. There are plenty of summaries of the numbers online, such as this concise article by Mark Vickery on Zacks. Today, I’m going to focus on a particular part of the Hewlett-Packard story: how and why the stock market consistently gets ahead of itself.

First let’s start out by getting some perspective on HPQ. So far in 2014, the stock has torn it up:

After the jump on Friday resulting from the positive earnings report, HPQ stock is now up over 30% in 2014. But let’s have another stiff dose of perspective, shall we?

In the past five years, while the stock market has nearly doubled, HPQ is down 17%. These struggles should come as no shock to most traders, as the printing and PC markets are certainly not what they once were.

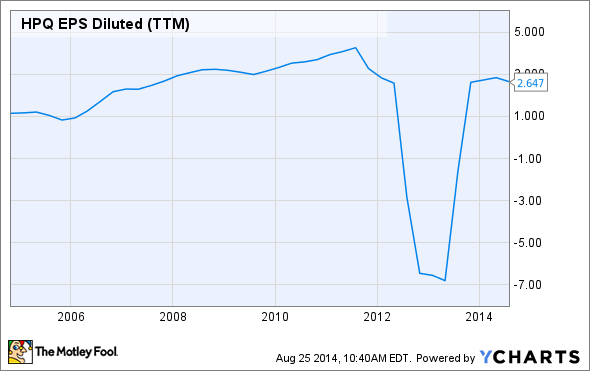

In fact, the PC world is dead, right? Printing is dead. Who owns a laptop anymore when there are iPads and Galaxy S’s? And who ever prints things anymore? What is this, the Stone Age? Clearly, HPQ must be hemorrhaging money at this point. I mean just take a look at its earnings:

Hmmm… actually that doesn’t look that bad. Especially when you take into consideration the lagging effect that the chaotic and ill-conceived plan to abandon the PC business had on the company several years ago. But ever since Hewlett-Packard placed former eBay CEO Meg Whitman in charge in 2011, the company has battened down the hatches and streamlined its operations to the point where its earnings appear to have stabilized for the time being.

However, despite this obvious recovery of the business and the 30% gain for the year, the stock still appears to be under-appreciated by traders. In fact, taking into account HPQ’s recent forward guidance, the stock’s forward P/E ratio remains below 10!

So what’s going on here? Why isn’t HPQ getting the respect it deserves? I believe the answer has to do with the fact that traders hold certain prejudices that have a real effect on share price. I hate to sound like a broken record, but despite the all the news and data that is available about a stock, at the end of the day there is only one way to move a stock price: traders must buy or sell the stock.

Now the word prejudice has lots of negative connotation to it. I’m using it strictly by it’s definition: “a preconceived opinion not based on reason.” And I want to be careful about using this word at all. The idea that a stock “should” be trading at a different price if only the rest of the market were as enlightened as I am is not only an egotistical way of thinking, it’s utterly useless when it comes to making money.

But these prejudices in the market are very real, and there are many examples of them. Back in 2009, I bought shares of then “Coinstar” (now “Outerwall“), owner of Redbox DVD vending machines. The early 2000’s marked a major transition in the home entertainment arena, and the inevitable result was the fall of Blockbuster and the rise of Netflix. Everybody knew that. I certainly did. I knew DVDs would end up being a thing of the past. However, I was aware of that idea when I bought Coinstar in 2009. I discussed my reasoning at length in my book:

I thought about my rural home town of Hazel Green, Alabama, and in 2009 I had a hard time imagining the typical Hazel Green resident streaming movies by connecting their HD TVs to Netflix on their laptops. I knew the transition was coming eventually, I just did not think that Hazel Green was ready quite yet. And I knew there were thousands of small towns and elderly people all across the country that are terrified of change and would cling to their DVDs until someone pried them from their cold, dead hands! So I believed that CSTR’s Redboxes had a multi-year window of expansion and growth during which the company could work on the eventual transition to online streaming.

It seems to me that the market has a major problem with transitional periods such as the one that occurred in the home movie sector a few years ago. Over the 3 1/2 years that I held Coinstar, I made over a 60% return on the stock, and yet when I sold it in February of 2013, it’s P/E ratio was still under 11! Talk about a lack of respect…

And it’s easy to see that Netflix is up nearly 1000% in the past five years. But it’s also easy to see that Netflix stock got way ahead of itself back in 2011 when it’s P/E ratio peaked at over 70 before the stock crashed 81% in a little over a year, dropping from around $275 down to $52. Many traders were dumbfounded by the move. Netflix is a great company, but in this case, the prejudice the market held was an over-appreciation of the stock. For the record, at $480 per share, Netflix’s current P/E ratio is about 144, nearly double its 2011 peak immediately prior to the 81% crash. Makes me wonder…

Traders get excited about stocks in emerging technology sectors such as electric cars (Tesla), streaming movies (Netflix), 3D Printing (3D Systems), and online retail (AMAZON!). And for many or all of these companies, the future is very bright. The disconnect, however, between the future of an industry and the future (particularly within a year or two time-frame) of a stock of a company within that industry can be staggering.

Maybe in ten years time we will not be printing ink on paper anymore, and computers will have gone the way of the rotary phone. But in the meantime, as long as Hewlett-Packard continues to rake in over $100 billion in annual revenue and its stock is trading at such a low forward P/E multiple, I will continue to be a shareholder.

Want to learn more about the psychology of the stock market? Or maybe you just want to be able to look sophisticated in front of your coworkers when they ask you what you are reading on your Kindle, and you’d prefer to tell them “Oh, I’m just reading a book about stock market analysis,” rather than the usual “Oh, I’m just looking at pics of my ex-girlfriend on Facebook.” For these reasons and more, check out my book, Beating Wall Street with Common Sense. I don’t have a degree in finance; I have a degree in neuroscience. You don’t have to predict what stocks will do if you can predict what traders will do and be one step ahead of them. I made a 400% return in the stock market over five years using only basic principles of psychology and common sense. Beating Wall Street with Common Sense is now available on Amazon, and tradingcommonsense.com is always available on your local internet!