A number of British stocks have been hit hard since the referendum vote to leave the EU, but Royal Dutch Shell (RDS.A, RDS.B) is not one of them. Shares are now up 0.3% since the Brexit vote after initially falling more than 8% during the knee-jerk market sell-off.

With the possibility that the Brexit could severely impact the British GDP growth in the coming years, Royal Dutch Shell offers a unique opportunity to invest in a company within a sector that is in a global upswing, a company that has significant international exposure and a company that is committed to maintaining the single largest dividend payment in the MSCI World Index.

Shell is in a position to grow FCF by dialing back capex without posing a threat to production. Furthermore, the company’s stable 6.6% yield is increasingly attractive to investors faced with European interest rates dipping into negative territory and U.S. Treasury rates dipping to their lowest level in history.

The company’s balance sheet is solid, and it has no serious near-term liquidity risks.

(Source: Shell)

What Are The Market’s Concerns?

The company’s stock remains down more than a third from its 2014 highs prior to the global oil market collapse, but it has bounced nearly 50% off of its January lows when oil dipped below $30/bbl. Clearly, many of the concerns the market had have eased in recent months, but it’s important to review them nonetheless.

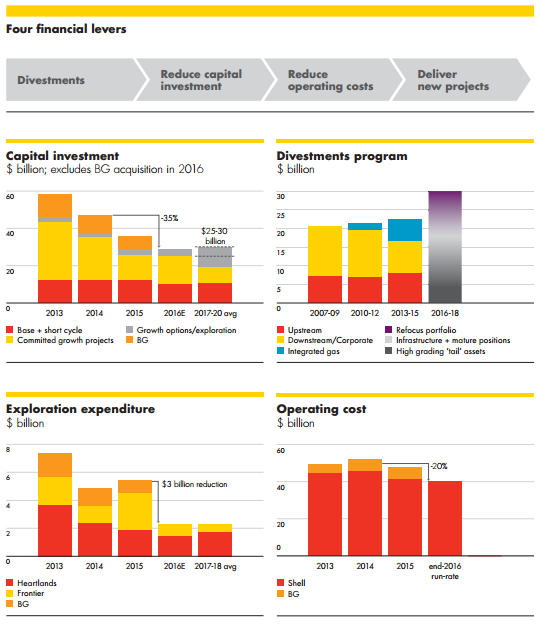

First, one of the company’s biggest selling points is its nearly 7% dividend yield. While the company hasn’t cut its dividend a single time in the past 70 years, there’s no question its balance sheet has been stretched incredibly thin during the oil downturn. The company compounded its budget woes with its $53 billion acquisition of BG Group as well.

Skeptical investors have questioned the acquisition and worried that the company has painted itself into a corner where it will have to choose between cutting the dividend and cutting production. However, management is addressing those concerns by planning to sell $30 billion in assets by the end of 2018 while maintaining current production levels.

Shell and BG combined to generate -$4 billion in FCF in 2015, and the company is on the hook for $15 billion in dividend payments by the end of 2016. However, despite the company giving no indication that it plans on cutting its dividend, the market seems to be pricing in a significant reduction in Shell’s dividend based on the stock’s yield prior to the downturn in the 4.75% to 5.5% range.

It seems as if one of two phenomena is at play: either the company will stray from its 70-year history of reliable dividend payments, or the stock is significantly undervalued.

I believe that Shell has a clear path to maintaining its dividend and increasing its FCF via BG synergies, capex reductions and asset sales. The company has yet to turn the quarter in terms of FCF. But once it does, the stock will likely see significant upside as it returns to its historical yield range.

In 2015, Shell generated roughly $30 billion in OCF, including $10 billion in asset sales. With capex of $26 billion and dividend payments of $12 billion, the company had to take on significant debt to make its dividend payments.

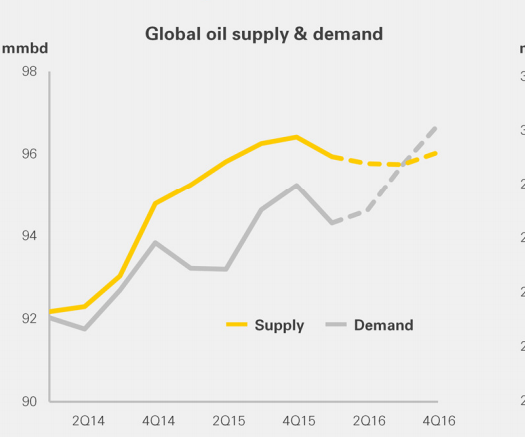

Management will continue to operate with the long-term goal of getting its payout ratio back down to its historical range between 50% and 100%. I believe it is on pace to get there by the end of 2017 even if oil prices remain as low as $45/bbl. Earlier this month, the US Energy Information Administration upped its 2017 price forecast for Brent crude from $49/bbl to $52/bbl.

(Source: BP)

Capex Cuts

The path to FCF recovery without a dividend cut for Shell involves…

Click here to continue reading

Want to learn more about how to profit off the stock market? Or maybe you just want to be able to look sophisticated in front of your coworkers when they ask you what you are reading on your Kindle, and you’d prefer to tell them “Oh, I’m just reading a book about stock market analysis,” rather than the usual “Oh, I’m just looking at pics of my ex-girlfriend on Facebook.” For these reasons and more, check out my book, Beating Wall Street with Common Sense. I don’t have a degree in finance; I have a degree in neuroscience. You don’t have to predict what stocks will do if you can predict what traders will do and be one step ahead of them. I made a 400% return in the stock market over five years using only basic principles of psychology and common sense. Beating Wall Street with Common Sense is now available on Amazon, and tradingcommonsense.com is always available on your local internet!